Fundamental information about the group

Organizational and management structure

thyssenkrupp AG is responsible for the strategic management of the group. In addition to governance tasks, the allocation of investment funds and management development, it concentrates especially on performance and portfolio management. Alongside the cross-cutting functions of strategy, human resources and finance that are within the remit of the Executive Board, responsibility for the segments is allocated to the individual Executive Board members. Especially in respect of operational management decisions, the individual segments act decentrally under the strong thyssenkrupp umbrella brand. The members of the Executive Board of thyssenkrupp AG are responsible for ensuring that the management teams achieve the performance targets.

The main administrative units for Germany, together with the individual corporate functions and the regional platforms (Regions) are combined in the Corporate Headquarters unit of thyssenkrupp AG. The Regions unit comprises four regional platforms: APA (Asia/Pacific/Africa), North America, South America and Greater China. In addition, our service units are combined at two companies – thyssenkrupp Services GmbH and thyssenkrupp Information Management GmbH – and provide cross-cutting services to the businesses and Corporate Headquarters. Most operations of thyssenkrupp Information Management GmbH were terminated on October 1, 2025. The IT tasks that were formerly this company’s responsibility were mainly transferred to external service providers.

In the course of transforming the thyssenkrupp group from an integrated industrial conglomerate into a financial holding company with investments in independent companies, we will also realign our Corporate Headquarters and service units. Corporate Headquarters is to become leaner and focus especially on the financial management of the segments. The service units will focus their portfolios on business-critical services for operations. Wherever it makes sense to do so, responsibility will be transferred to the segments.

Sales regions and customer groups

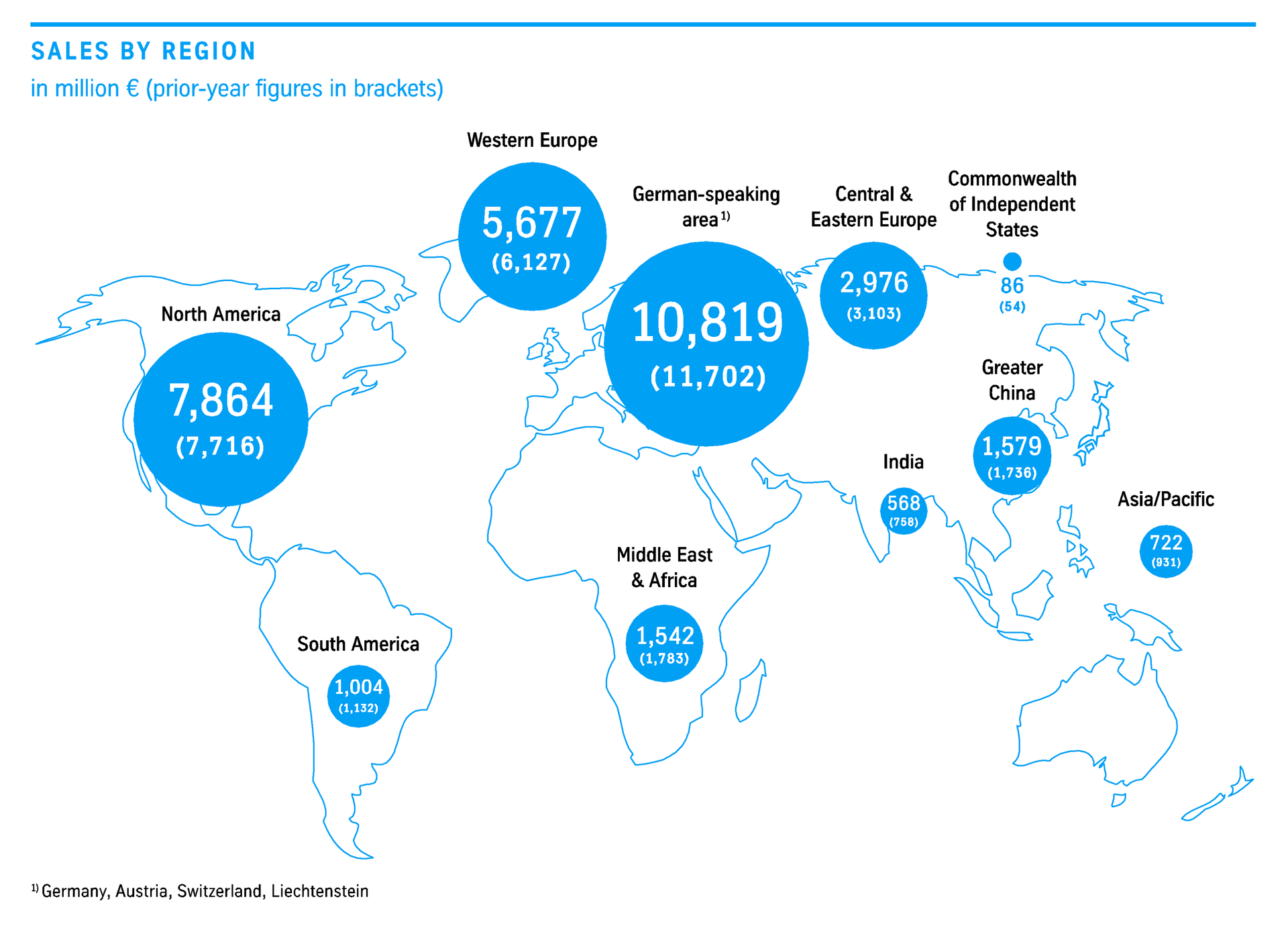

In the reporting year, the German-speaking region (Germany, Austria, Switzerland and Liechtenstein) was once again our most important sales market, accounting for sales of €10.8 billion. It was followed by the business with North America (€7.9 billion) and business with customers in Western Europe (€5.7 billion). Sales in Greater China amounted to €1.6 billion.

The automotive industry remained the most important customer group with a sales share of 33%; it is particularly important for our automotive components and commercial vehicles activities and our steel business. It was followed by trading, steel and related processes and the remaining parts of the processing industry. Other key customer groups were engineering, the public sector (defense), the packaging industry, energy and utilities, and the construction industry.

Targets and strategy

Together with our customers, we want to use our extensive and long-standing expertise in innovating technologies to develop cost-effective, resource- and environment-friendly solutions to the challenges of the future. By bringing together our innovative products, technologies and services under the roof of a strong umbrella brand, we want to make a contribution to a better, more livable and more sustainable future. We focus on forward-looking solutions and aim to assume responsibility by achieving progress coupled with effectiveness.

Financial targets

In an environment that remains geopolitically and economically challenging, we are seeking a tangible increase in the operational performance of all our businesses, thereby establishing the basis for thyssenkrupp to generate sustained positive value and cash flow contributions. Our goal is for our businesses to achieve the financial targets that have been defined for the medium term.

On the basis of the current portfolio structure, we are adhering to the medium-term targets for the group as communicated in the last Capital Market Update 2022 and the Annual Report 2022 / 2023: an adjusted EBIT margin of 4% to 6% and a significantly positive free cash flow before M&A. The reliable payment of a dividend remains a primary target.

Automotive Technology – Adjusted EBIT margin of 7% to 8%

Decarbon Technologies – Adjusted EBIT margin of more than 5%

Materials Services – Adjusted EBIT margin of 2% to 3%

Steel Europe – Target for adjusted EBIT margin subject to the business plan being prepared

Marine Systems – Adjusted EBIT margin of >7%

Further information about segment performance and target achievement can be found in the subsection headed “Segment review” in the “Report on the economic position.” Details of the performance indicators can be found in the “Corporate management” subsection. The forecast for the current year is presented in the “Forecast report.”

Group strategy

thyssenkrupp is driving forward with its strategic realignment. In May 2025, we communicated a model for the future alignment of the group. At the core of this target concept is the stepwise transition of all thyssenkrupp’s businesses to stand-alone solutions that are open to third-party investment. thyssenkrupp AG is to be transformed into a financial holding company that serves as the umbrella for majority investments in strong and independent companies – with clear roles, independent management and their own contribution to value added.

The strategic alignment is focused on leveraging the opportunities harbored by key future-oriented areas with significant growth potential. Environmental issues play a central role here. On the path to climate neutrality, hydrogen technologies, green chemicals, renewable energy, e-mobility and supply chains are relevant focus areas. In implementing our strategy, we remain committed to three main areas of action: portfolio, performance and green transformation.

Portfolio

A clear decision has been taken on the direction of thyssenkrupp: We want every individual business to develop in the best possible way and to achieve a sustainable competitive position. We are convinced that establishing an independent organization for the segments – with the advantage of their own access to the capital markets and the option for third-party investment – will enable them to leverage their full value potential and use their independence to make investments, access market opportunities and achieve further growth. However, the starting position for a stand-alone solution differs from segment to segment, depending on the market environment, business model and progress in transformation. In preparing this step, the businesses are therefore setting different accents, moving at different speeds and considering different measures.

Automotive Technology is to evolve into a focused and high-growth automotive supplier in a stand-alone configuration. Since October 1, 2025, the segment has been realigning its activities into four customer- and technology-focused business units. This reorganization is intended to create simplified structures, increase innovative strength and enable synergies. In addition, the aim is to establish the conditions for actively contributing to the transformation of the automotive industry. The goal is to create a profitable and clearly positioned segment that benefits particularly from the structural growth of the e-mobility sector and the Asian markets. At the same time, Automotive Technology is adjusting its portfolio. The Automotive Body Solutions, Automation Engineering and Springs & Stabilizers business units are now being managed separately and we are exploring strategic options such as partnerships or new ownership models. In this context, with the signing of the corresponding agreements, we initiated the sale of the Automation Engineering core business to Agile Robots on November 21, 2025.

Decarbon Technologies is aligning its business model with growth in the field of climate-relevant technologies. The goal is to further increase its innovative strength and facilitate access to specialized, industry-specific investors, focusing on market-relevant future fields such as hydrogen, Carbon2Chem and industrial decarbonization. The business is continuing to develop dynamically to leverage these market opportunities, specifically expanding the expertise, partnerships and technological platforms necessary to achieve this.

With its vision of “Materials as a Service,” Materials Services is evolving into a data-driven provider of materials and logistics services focused on expanding digital platforms, sustainable logistics solutions and high-growth business areas. The lean business unit structure introduced in July 2024 is intended to strengthen efficiency and customer focus, creating the basis for forward-looking strategic development.

Steel Europe continues to implement the industrial future concept, thus responding to structural changes in the markets. This is aimed in particular at optimizing the production network in combination with a reduction in production capacities to increase the segment’s competitiveness and profitability. In parallel, we will continue to implement the existing Strategy 20–30 to improve the segment’s operating performance. At the start of April 2025, thyssenkrupp Steel Europe AG terminated the supply agreement with HKM, ending its obligation to purchase around 2.5 million tons of steel each year as of December 31, 2032. In July 2025, we reached consensus with the IG Metall trade union on the new “Steel Realignment” collective restructuring agreement, thus fulfilling a key condition for the long-term competitiveness and successful positioning of thyssenkrupp Steel. Moreover, in mid-September 2025, a non-binding indicative offer was received from Jindal Steel International for the acquisition of thyssenkrupp Steel Europe. This is being reviewed by thyssenkrupp AG with regard to economic viability and the continuation of the green transformation. In this connection, EP Group (EPG) and thyssenkrupp AG mutually agreed to end their negotiations on a possible 50 / 50 joint venture for thyssenkrupp Steel Europe. As of September 30, 2025, EPG returned the 20% interest it had acquired in thyssenkrupp Steel Europe AG on July 31, 2024 and received reimbursement of the purchase price.

Since October 20, 2025, TKMS (Marine Systems segment) has operated as an independent, publicly listed systems supplier in the maritime defense market. This move has not only strengthened the financial independence of TKMS but provides the company with new opportunities for growth and innovation. At the same time, thyssenkrupp AG remains the strategic majority shareholder with an interest of 51%, thus ensuring stability. The transaction marks an important step in the group’s transformation into a financial holding company.

Performance

The goal of the transformation process is to sustainably boost the performance and competitiveness of all our businesses, achieve a positive free cash flow before M&A and establish the basis for paying a reliable dividend. The condition for this is that the businesses achieve their financial targets rapidly and in the long term, even in challenging conditions (see the subsection headed “Financial targets”).

In September 2023, thyssenkrupp launched the groupwide APEX performance program. This consolidates the group’s existing and newly developed transformation and performance measures aimed at improving the profitability and market opportunities of all its businesses. In the first phase, measures were identified in respect of assets/CAPEX, business models and sales, material costs, net working capital and organization. They are currently being implemented.

The second phase of the program is focused on structural measures to improve efficiency, optimize business models and adapt to the markets. Our goal is to consistently implement the necessary restructuring measures. As this phase progresses, it is planned to decentralize management of the measures although the central APEX Transformation Office will continue to provide support. Responsibility for the implementation and success of the measures lies with the individual businesses.

Details about progress in implementing the measures can be found in the subsection headed “Segment review” in the “Report on the economic position.”

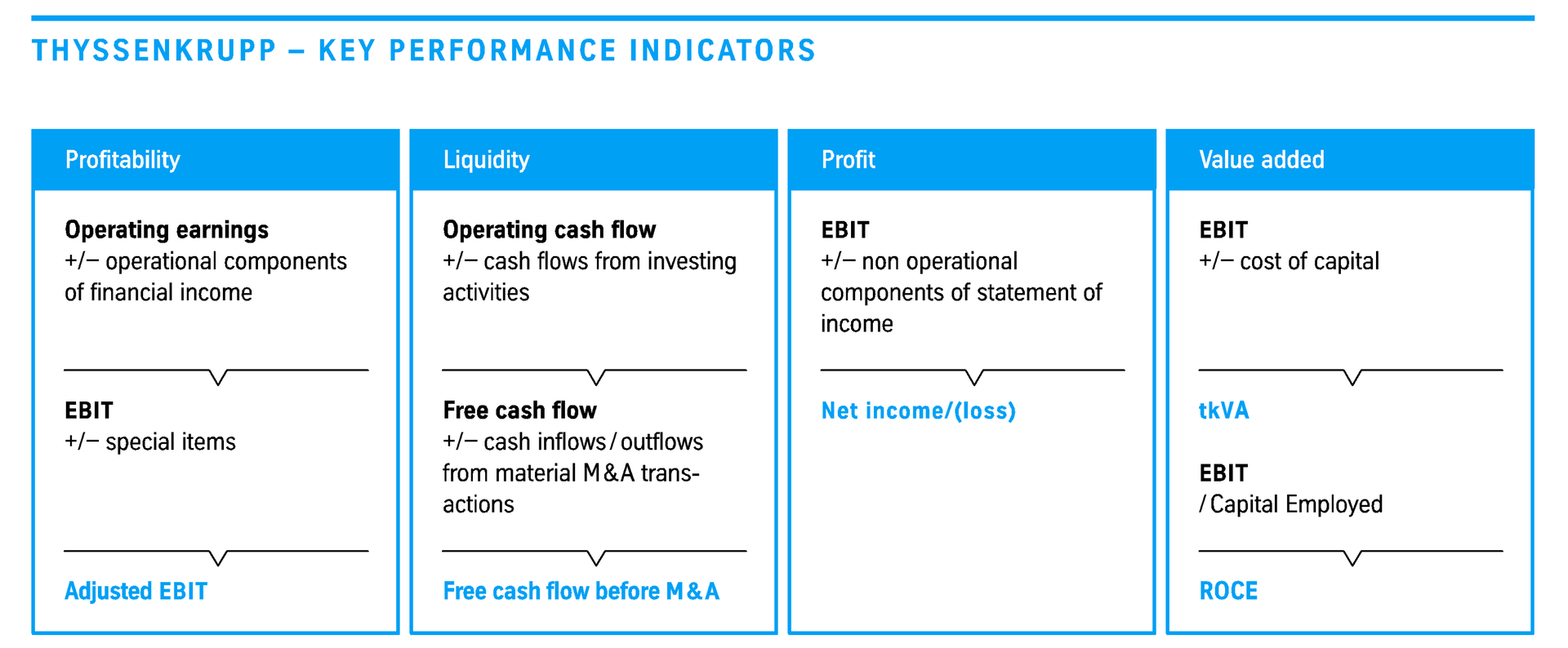

Adjusted EBIT

EBIT provides information on the profitability of a unit. It contains all elements of the income statement relating to operating performance. These include items of financial income/expense that can be characterized as operational, including income and expense from investments where there is a long-term intention to hold the assets. The thyssenkrupp group has an investment in the former Elevator Technology segment. This investment has no strategic or operational connection to the group’s continuing operations. The corresponding expenses and income are not included in financial income/expense from operations and therefore also not in EBIT. Adjusted EBIT is EBIT adjusted for special items such as measures in connection with restructuring, impairment losses/impairment reversals on non-current and current assets, disposal gains or losses and income and expenses in connection with the CO2 forward contracts of the Steel Europe segment. It is more suitable than EBIT for comparing operating performance over several periods.

The adjusted EBIT of the group and the segments and the special items are described in the “Analysis of the results of operations of the group” and “Segment review” subsections in the “Report on the economic position.” Please also refer to the reconciliation in the segment reporting (Note 24).

Green transformation

Our goal is to use our innovative products and state-of-the-art digital technologies to provide substantial support to our customers in the green transformation and achieving their sustainability targets. Thanks to its broad technology portfolio, the Decarbon Technologies segment is making a contribution to the sustainable transformation of energy-intensive industries. The segment identifies major decarbonization trends such as those in the areas of hydrogen (majority investment in thyssenkrupp nucera), green chemicals (Uhde), cement (Polysius) and renewable energy (Rothe Erde). These areas are strategically well positioned to benefit in the medium and long term from the substantial growth potential associated with the green transformation. Examples of green technologies are described in the subsection headed “Technology and innovations.”

Alongside the products and solutions whose development we are driving forward for our customers, we are working on the decarbonization strategy of our own group. Through Steel Europe’s hydrogen-capable direct reduction plant, currently under construction, we are aiming to cut annual CO2 emissions by as much as 3.5 million tons. This project is strengthening thyssenkrupp’s role as a major purchaser in the European hydrogen economy and making Duisburg an important hydrogen infrastructure site. At the same time, the group is pursuing economic routes with the long-term target of climate neutrality.

Management of the group

The indicators used throughout the group for profitability, liquidity, profit and value added form the basis for operational and strategic management decisions at thyssenkrupp. We use them to set targets, measure performance and determine variable components of management compensation – in addition to other factors. For us, the most important financial indicators are adjusted earnings before interest and taxes (adjusted EBIT), free cash flow before mergers and acquisitions (FCF before M&A), net income/(loss) of the thyssenkrupp group and thyssenkrupp Value Added (tkVA) or the return on capital employed (ROCE).

The Executive Board also defines primarily long-term targets for the segments. These form the framework for the short- and medium-term financial targets and also for the budget and medium-term plans, which are prepared by all units.

FCF before M&A

FCF before M&A permits a liquidity-based assessment of performance in a period by measuring cash flows from operating activities excluding income and expenditures from material portfolio measures. It is measured as operating cash flow less cash flows from investing activities excluding cash inflows or outflows from material M&A transactions. This too links more directly to operating activities and facilitates comparability in multi-period analyses.

From fiscal year 2025 / 2026, the addition of right-of-use assets under leases (in accordance with IFRS 16) will no longer be recognized as an investment in the FCF before M&A performance indicator. In the future, the actual lease payments – comprising the repayment and interest components – will be included in the calculation of cash flows.

A reconciliation and details on the development of FCF before M&A are provided in the analysis of the cash flows in the subsection headed “Analysis of the financial position of the group” in the “Report on the economic position.”

Net income/(loss)

Net income is the profit generated by the group in the fiscal year. It is calculated as a positive balance of all income and expenses. Unlike EBIT, the calculation includes non-operating items, for example, interest and taxes. Net income therefore provides information on the group’s earning power. Negative net income is referred to as a net loss.

The net income/(loss) of the thyssenkrupp group is explained in detail in the subsection headed “Analysis of the results of operations of the group” in the “Report on the economic position.”

tkVA / ROCE

tkVA is the value created in a reporting year. This indicator enables us to compare the financial performance of businesses with differing capital intensity. tkVA is calculated from the EBIT less the cost of capital employed in the operating business. Capital employed mainly comprises fixed assets, inventories and receivables. Deducted from this are certain non-interest-bearing liability items such as trade accounts payable. To obtain the cost of capital, capital employed is multiplied by the weighted average cost of capital (WACC), which includes weighted equity and debt. We use the return on capital employed (ROCE) to determine the relative return generated. ROCE is the ratio of EBIT to capital employed. If ROCE exceeds WACC, i.e., the returns due to shareholders and lenders, we have created value.

Information on the development of tkVA / ROCE in the reporting year can also be found in the subsection headed “thyssenkrupp Value Added (tkVA)” in the “Report on the economic position.”

Technology and innovations

Innovation strategy

With their experience and know-how, the companies in the thyssenkrupp group can develop solutions for the challenges of the future. Here, a key role is played by the green transformation of industry.

We conduct our research and development activities with around 3,900 employees. In many cases, this is done in collaboration with external partners such as universities, research institutes and other industrial enterprises. In the reporting period we registered around 1,420 new patents and utility models. As of the reporting date, our patent portfolio therefore contained some 16,870 patents and utility models and the trademark portfolio around 9,490 property rights.

Total spending on research and development came to around €695 million in the reporting year, an increase of about 1% compared with the prior year (€690 million). The adjusted R&D intensity was 3.2% (prior year: 2.9%) and therefore in the company’s target range of around 3.0%; this figure refers to R&D costs as a proportion of sales, without trading and distribution.

In fiscal year 2024 / 2025, we capitalized development costs of €48 million (prior year: €35 million). The capitalization ratio – capitalized costs as a proportion of overall R&D costs – was therefore 16% (prior year: 12%).

Innovation for the green transformation

We are continuing to drive forward the green transformation in respect of our own processes. We also deliver many innovative solutions that offer our customers support in implementing their own climate- and resource-saving processes and introducing more sustainable products.

The most prominent example of the transformation of our own processes is our target of climate-neutral steel production by 2045 at the latest. The key element in achieving this target is the construction of our first hydrogen-capable direct reduction plant. Further information can be found in the subsection headed “Targets and strategy” and in the sustainability report.

Today, thyssenkrupp already offers technological solutions for the entire green hydrogen value chain. A particular highlight is thyssenkrupp nucera’s technology portfolio for the industrial-scale production of hydrogen using electrolyzers.

Uhde and Uniper have entered into a strategic partnership to develop the ammonia cracker to industrial maturity as a key technology for hydrogen transport and trade worldwide. The ammonia cracker splits ammonia catalytically into its two constituents – hydrogen and nitrogen. The goal of the collaboration is to use imported ammonia on an industrial scale to produce hydrogen for use by the energy, steel and chemical industries, among others. Using ammonia as a transport and storage medium makes it possible to produce large quantities of green or low-carbon hydrogen at sites around the world. It is the condition for ramping up the global hydrogen economy. In a first step, the two project partners aim to construct a demonstration facility with a daily capacity of 28 tons of ammonia at the site in Gelsenkirchen-Scholven, Germany. The project is receiving financial support from the State of North Rhine-Westphalia.

Cement production accounts for around 7% of greenhouse gas emissions worldwide so switching to climate-friendly processes is very important. The calcination of limestone is a key step in the production of lime and cement that emits large quantities of CO2. We have signed a letter of intent with a Swedish company to conduct a joint pilot project with the goal of electrifying this process step. Polysius is to supply the kiln system for a novel lime production facility that is to be constructed at a site in Norway. The planned facility is based on the innovative Electric Arc Calciner (EAC) technology developed by the Swedish partner. It electrifies the calcination process that has traditionally used fossil fuels, thus reducing CO2 emissions from lime production. If the electricity required is generated from renewable sources, this part of the process is almost entirely emission-free.

The Carbon2Chem® collaborative project has been awarded funding of €50 million from the German Federal Ministry of Education and Research for the third project phase through to the end of 2028. The project focuses on how the blast furnace gases emitted during steel production can be converted into valuable chemical starting products used for fuels, plastics and fertilizers, among other things. The third phase of the collaboration will include the application-based verification of the technical solutions and the comprehensive study of the quality of methanol and hydrogen – both during production and storage. A new generation of electrolyzers will be developed. The research work will also be expanded to explore new value chains such as sustainable aviation fuels.

Profile and organizational structure

Overview

thyssenkrupp is an international industrial and technology group with around 93,400 employees. In 48 countries, our companies achieved sales of €32.8 billion in fiscal year 2024 / 2025.

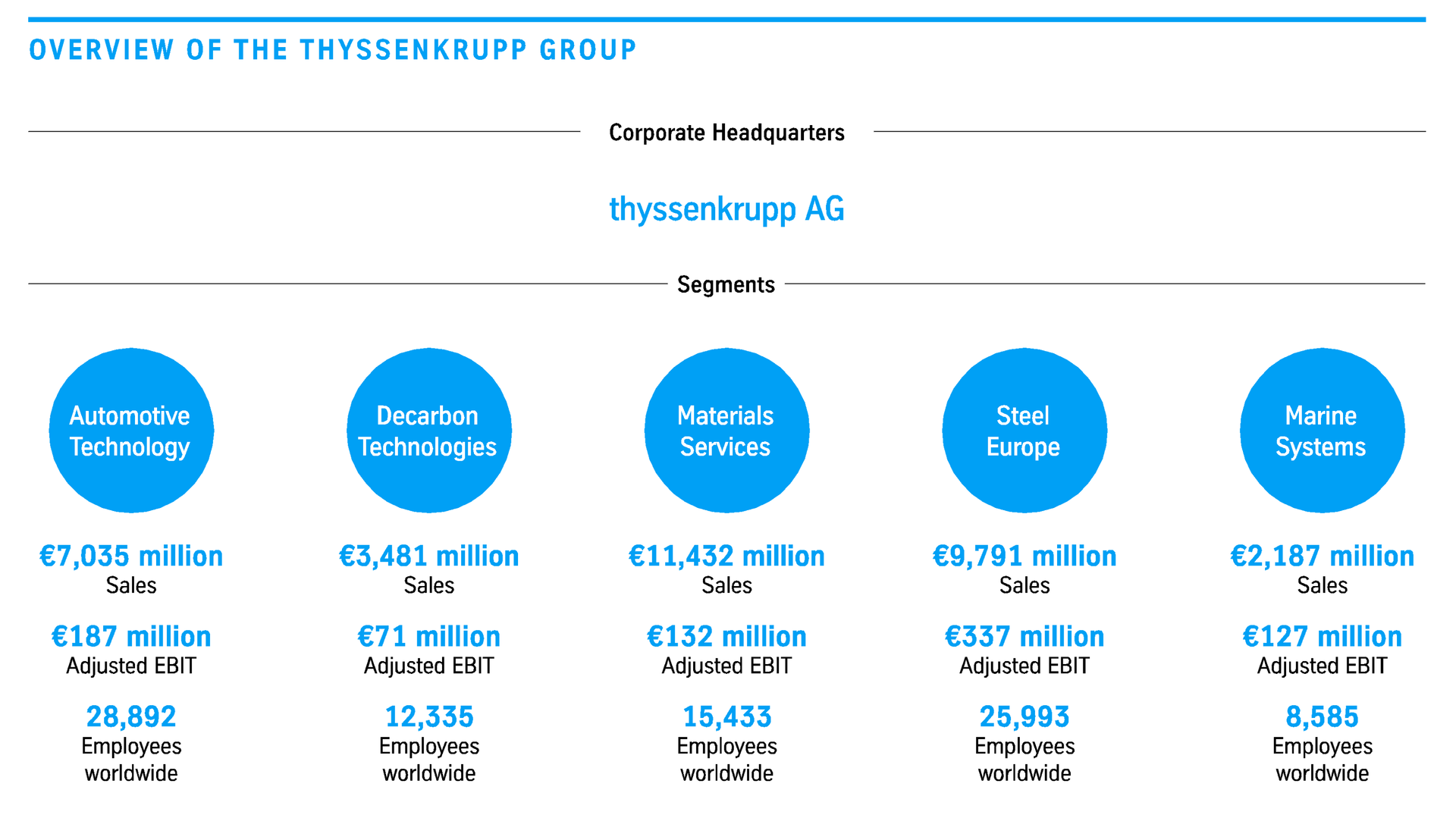

In the reporting year, our business activities were organized in five segments: Automotive Technology, Decarbon Technologies, Materials Services, Steel Europe and Marine Systems. On October 20, 2025, TKMS (Marine Systems segment) became an independent, publicly listed company; thyssenkrupp AG holds the majority investment of 51%. The segments are generally divided into business units and operating units.

As of September 30, 2025, 320 companies and 15 investments accounted for by the equity method were included in the consolidated financial statements.

Our high standards and shared values are documented in our mission statement, which can be found on our website.

Our segments are active in the following areas:

Automotive Technology is one of the larger German suppliers and engineering partners to the international automotive industry. Its product and service portfolio comprises high-tech components, systems and automation solutions for vehicle manufacturing, as well as mechatronic solutions based on electronics and internally and externally developed software. We also produce forged components and systems for a wide range of customer applications in the construction machinery and mobility sectors.

Through its Rothe Erde, Uhde and Polysius businesses as well as the majority investment thyssenkrupp nucera, Decarbon Technologies delivers innovative, cutting-edge technologies for the transition to a climate-neutral industrial economy. Rothe Erde is a leading provider of bearings and solutions that play a key role in wind, solar and tidal power plants, among other things. With its solutions for decarbonization, defossilization and the circular economy, Uhde is a technology and implementation provider of large-scale plants for the chemical industry. Polysius supplies green technologies for the cement and lime industry, digital automation solutions, and on-site and remote maintenance services. thyssenkrupp nucera is a global supplier of electrolysis technology for the industrial-scale production of clean hydrogen.

Materials Services is one of the world’s leading materials distributors and service providers. In this segment, we offer our customers not only a wide range of materials and raw materials but also the associated services – ranging from processing options and supply chain management to warehousing and logistics. Thanks to our extensive network of sites, we are present where our customers need us. Our core markets are North America and Europe. The customers of the Materials Services segment are found in manufacturing sectors such as aerospace, infrastructure, automotive, machinery and metal processing, as well as in trading and data centers.

Steel Europe is Germany’s largest steel producer, focusing on the manufacture of high-quality flat carbon steel. Its product portfolio comprises hot-rolled coil, sheet steel, premium cut-to-length sheets, coated products, tinplate, medium coil and both grain-oriented and non-oriented electrical steel in a wide range of grades – available in all cases as both conventional and CO2-reduced products. The main purchasers of the products are the automotive and engineering sectors, the energy sector, the metal processing industry and the construction industry. We see our strengths in the development of customized solutions and in our technical know-how, which is based on many years of experience.

Marine Systems is one of the world’s leading suppliers of system solutions for maritime defense applications. As a fully integrated system supplier, the segment develops and builds conventional submarines and naval vessels at its three shipyard sites in Kiel, Wismar and Itajaí (Brazil). It also produces unmanned systems, sensors, sonar systems, effectors, software solutions and maritime guidance systems at sites in Germany and the United Kingdom, for example. The new and independent TKMS brand will propose holistic solutions from a single source, ensuring our customers’ defense capability through the interaction of surface and submarine solutions and comprehensive service that spans the product life cycle.