Strategy

ESRS 2 SBM-3 – Material impacts, risks and opportunities and their interaction with strategy and business model

The following explains the material impacts, risks and opportunities in connection with climate change that were identified by the materiality assessment performed and are significant to thyssenkrupp’s operations and business model.

1) I = impact; (-) = negative; (+) = positive; R = risk; O = opportunity

2) VC = value chain; U = upstream; Op = own operations; D = downstream

3) TH = time horizon; S = short-term; M = medium-term; L = long-term

Resilience analysis of the strategy and business model in respect of climate change

In the 2024 / 2025 reporting year, the company performed a scenario analysis in order to systematically identify material climate-related risks and opportunities, as well as their potential impacts on the strategy and business model. This analysis integrates the findings of the double materiality assessment and is oriented toward the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD) in that it covers the approach for including governance, strategy, risk management, metrics and targets, and transition and physical risks

Transition climate risks and opportunities

The analysis of the transition climate risks and opportunities was performed on the basis of a company-specific combined scenario. It is based on the Net-Zero-by-2050 scenario of the International Energy Agency (IEA; 2021) as the leading reference pathway, supplemented by content from the EU 1.5Tech reference scenario for technological aspects and by findings from the IPCC’s SSP1-1.9 (AR6) scenario to address the limitations of the leading IEA scenario, especially its global aggregation level, the focus on transition rather than physical climate risks and the highly standardized assumptions with no probability of occurrence. The orderly transition scenario is aimed at limiting global warming to 1.5 degrees Celsius and reducing net emissions of greenhouse gases to zero by 2050 with the aid of ambitious climate policy, technological innovation and far-reaching transformation processes. The leading scenario is in line with thyssenkrupp’s GHG reduction targets, which have been assessed by the Science-Based Targets initiative (SBTi) and, due to the orderly decarbonization pathway based on technological innovation, is suitable for identifying material transition risks and opportunities associated with the green transformation. Although the IEA published an updated net zero roadmap in 2023, the 2021 net zero scenario continues to be recognized by science and industry as an international reference pathway that is consistent with 1.5-degree Celsius compatibility and thus represents the current state of the art. Moreover, the central assumptions and development pathways of this scenario are compatible with the climate-related assumptions that underpin the investment calculations chosen by the group and the assessment of climate-related financial risks. In particular, the regulation-driven increase in external carbon pricing in the reporting period reflects the shadow carbon price used in financial assessments (see subsection “E1-8”).

The analysis examines two time horizons: 2030 as the medium-term horizon that includes the intermediate targets of reducing emissions in line with the 1.5-degree Celsius target of the Paris Climate Agreement and 2050 as the long-term horizon reflecting global net zero ambitions. The focus of the analysis was the 2030 time horizon, which is in line with thyssenkrupp’s intermediate targets on its path to net zero emissions. For the long-term horizon through 2050, the analysis is associated with greater uncertainties. Due to the information available at the reporting date, there is only a limited possibility of reliably quantifying climate-related risks and opportunities. For this reason, the statements were restricted to an overarching level. Moreover, the reliability of the information is subject to uncertainties in respect of social developments, technological pathways and customers’ willingness to make final investment decisions (FID), as well as other external impact drivers.

Potential climate-related transition events that might be significant were identified along the value chain. These include political, economic and technological changes that might have an impact on business activities, markets and supply chains. The transition events were assessed qualitatively in respect of the probability of their occurrence and impacts. Leading sustainability experts from the segments participated in identifying and assessing the events. The findings were aggregated at group level, where they underwent a final assessment and prioritization.

The analysis identified material transition risks in several areas such as regulatory risks in connection with carbon pricing by, for example, the EU Emission Trading Scheme (EU ETS), as well as infrastructure and economic risks relating to the expansion of the hydrogen economy. In addition, demand-side uncertainties were identified as material transition risks in relation to market acceptance – especially regarding the willingness to pay for products with a lower carbon content than conventional products, which are being limited by growing competitive pressure. Other risks were identified that might occur in the downstream value chain, especially as the result of customer reticence to invest – with corresponding impacts on thyssenkrupp’s market opportunities – and the risk that neutralization technologies for carbon capture and storage or use are not recognized as options for reducing GHG emissions. The security of supply with critical starting products and materials is also a transition risk.

At the same time, material climate-related opportunities were identified in connection with the industrial transition to a decarbonized economic system. With products and technologies that facilitate low-emission manufacturing, such as CO₂-reduced steel, electrolyzers for renewable hydrogen, processes for the basic material and chemical industries and system components for the generation of renewable energy, thyssenkrupp can position itself as a provider of solutions for lower-carbon industrial value chains. These areas harbor new sales and earnings potential for thyssenkrupp and, at the same time, could strengthen the company’s brand value and enable it to access new customer groups and safeguard jobs.

Physical climate risks

The scenario analysis examined physical climate risks as well as transition risks. This assessment covered both acute and chronic risk types, including flooding, water and heat stress, storms and coastal erosion in accordance with the classifications of physical climate risks contained in the EU Taxonomy (Delegated Regulation (EU) 2021/2139, Appendix A) and ESRS E1. The analysis of physical climate risks performed as part of the resilience analysis is applied to the company’s operating sites and does not include the upstream and downstream value chain.

A structured four-step methodology was used for the analysis, in line with the requirements of the EU Taxonomy and ESRS 2 IRO-1. It was based on high-resolution climate projections from the CMIP6 model set, taking account of various emission and development pathways, including RCP2.6, RCP4.5, RCP6.0 and the particularly emissions-intensive SSP5-8.5 / RCP8.5 scenario, combined with geospecific risk data. These include spatially resolved, site-related information on the probability, intensity and evolution of climate risks over time, based on locally projected climate scenarios and regional risk models. A time horizon until 2055 was examined. In the first step, the vulnerabilities specific to a site and activity were assessed on the basis of structured indicators – for example, relating to construction features, critical infrastructure and the industry-specific classification of an economic activity. Where there were gaps in the data, a conservative medium to high value was assumed so that risks were not underestimated. In the second step, climate-related risks were assessed on the basis of the aforementioned climate projections; this assessment covered both acute risks such as flooding, heat waves and storms and chronic risks such as long-term temperature increases, water stress and soil degradation in terms of their probability of occurrence, intensity and development over time. In the third step, a standardized assessment formula was used to translate the findings for vulnerability and risk into a site-specific climate risk indicator on a standard scale from 0 to 1; the findings were classified in six risk levels ranging from zero to very high, reflecting the highest risk identified for each site. In the fourth step, specific adaptation recommendations were derived for the sites with a high or very high risk. These recommendations are aligned with the risk type and the local economic activity; priority is given to nature-based solutions and green infrastructures.

As a result of this analysis, 57 sites with at least one elevated physical climate risk were identified; one of these is a site with a very high risk. Physical climate risks particularly affected sites in:

Coastal regions with a high risk of flooding and coastal erosion

Central, Southern and Southwestern Europe with an elevated risk due to water stress

Central Europe with an elevated risk due to drought

Sites worldwide with an elevated risk due to river flooding

As part of the analysis, specific adaptation recommendations were prepared for the affected sites. These recommendations focused on the type of risk identified and on the respective economic activity. The adaptation recommendations include, for example:

Flood protection measures (e.g., local barriers, drainage systems)

Strategies for cooling and reducing heat in buildings

Water-related adaptations in regions at risk of water stress

Assessments of medium-term adaptability (e.g., modernization) at sites

However, the specific necessity for implementing such adaptation recommendations must be assessed for each site on the basis of further reviews and validation.

A time horizon until 2055 was applied in analyzing physical climate risks. This is compatible with the time horizons until 2030 and 2050 used in the analysis of transition risks and opportunities and with the GHG reduction targets for these years in accordance with subsection “E1-4.”

The method for analyzing physical climate risks displays limitations. Although the CMIP6 climate models used (RCP2.6–RCP8.5) deliver high-resolution projections, they reflect regional and local context factors to only a limited extent. Site-related vulnerabilities are assessed on the basis of standardized indicators. Where there are gaps in the data, conservative assumptions are made, which may limit the accuracy. The analysis is a snapshot of a given moment that does not take account of either dynamic changes in future scenarios or financial impacts; it covers only the company’s own operating sites, but not the upstream and downstream stages in the value chain.

Resilience of the strategy and business model

The goal of the scenario analysis was to assess the resilience of the corporate green transformation strategy in respect of climate-related risks and its ability to leverage opportunities. The analysis showed that the strategy is resilient overall but that critical success factors for its implementation are the economic availability of renewable hydrogen and the development of sales markets for products with a lower carbon content than conventional products and for technologies that are themselves low-emission or facilitate emission reductions.

thyssenkrupp is pursuing the goal of achieving net zero emissions by 2050 at the latest and is aligning with the 1.5-degree Celsius target of the Paris Climate Agreement to achieve this. The transition plan for climate change mitigation is embedded as a central element of the corporate strategy and serves as an instrument for achieving this goal. Among the main actions are the establishment of hydrogen-capable steel production, the development and marketing of products with a lower carbon content than conventional products and of technologies that are themselves low-emission or facilitate lower emissions, and collaborations with suppliers to decarbonize the supply chain. These actions are aimed at strengthening the resilience of the business model.

At thyssenkrupp, physical climate risks are additionally addressed in the context of insurance-related risk management, which covers risk avoidance and mitigation measures alongside risk transfer mechanisms. In this context, structured hedging and provisions serve to increase both organizational and financial resilience. Further information on insurance-related risk management can be found in subsection “E1-2.”

E1-1 – Transition plan for climate change mitigation

The transition plan for climate change mitigation is the main instrument for implementing thyssenkrupp’s climate strategy. It serves as the operating framework for the stepwise decarbonization of the company across its value chain and includes ambitious GHG reduction targets. The paragraphs below describe the targets, actions, progress and financial resources for the transition plan.

Compatibility with the 1.5-degree Celsius target of the Paris Climate Agreement

The transition plan for climate change mitigation is compatible with the target of restricting global warming to 1.5 degrees Celsius, as specified in the Paris Climate Agreement. This is based on the planned attainment of net zero emissions groupwide by 2050 at the latest and the definition of science-based intermediate and long-term targets. The reduction targets for Scope 1, 2 and 3 GHG emissions set in the context of the transition plan were analyzed by SBTi and satisfy the requirements in terms of timing and ambition as defined in the current Corporate Net-Zero Standard. In June of the 2024 / 2025 reporting year, the transition plan target system was assessed by SBTi to be compatible with the 1.5-degree Celsius pathway. Further information on the GHG reduction targets can be found in subsection “E1-4” and “E1-6.”

Decarbonization and central actions

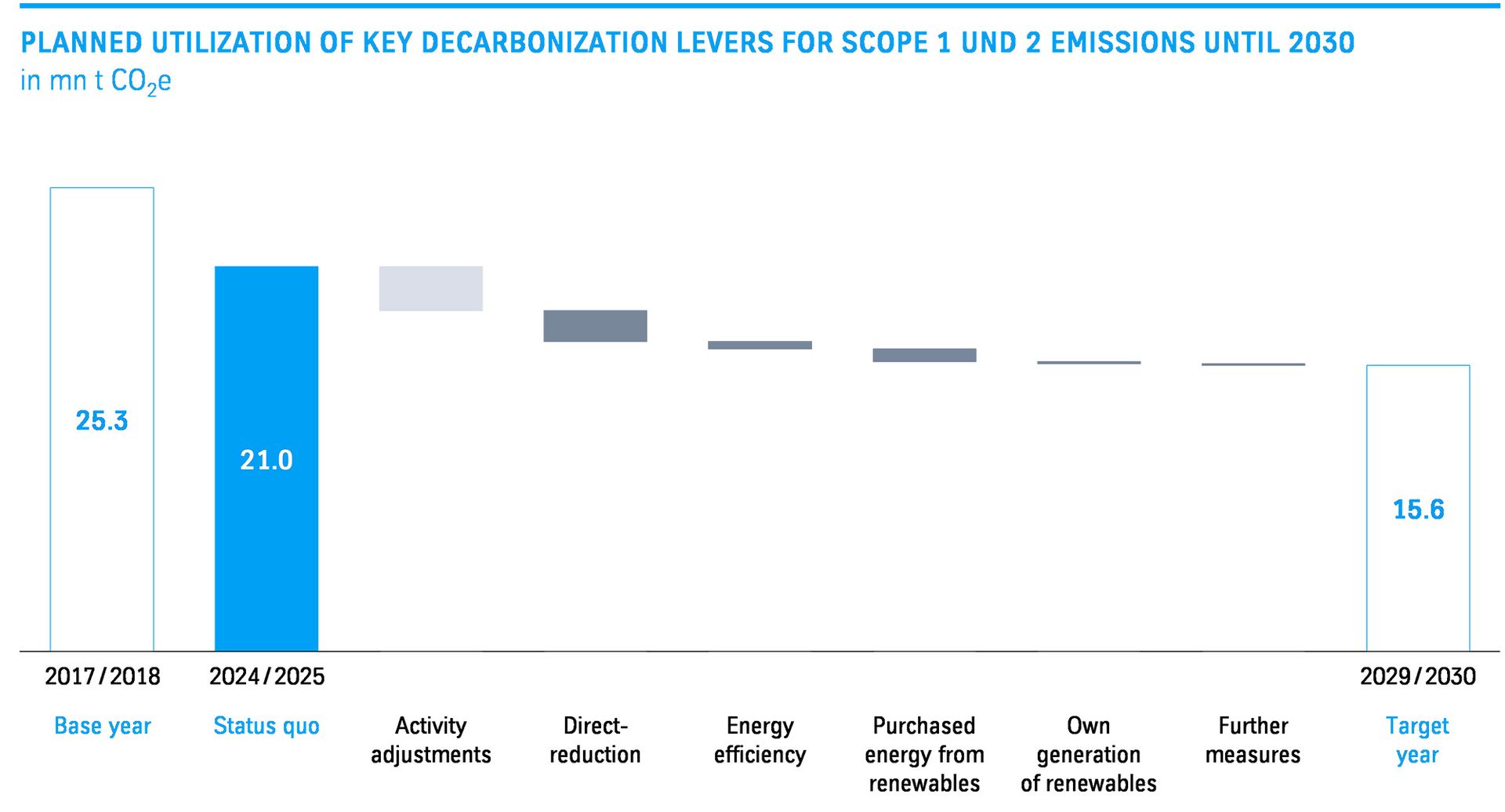

The main lever for reducing GHG emissions in the company’s own operations is the transformation of steel production, especially by constructing and operating a fully hydrogen-capable DR plant. Other key decarbonization levers for the company’s own operations include actions to increase energy and process efficiency, the switch of third-party energy supply to renewable sources and the company’s own generation of renewable energy. The adaptation of production volumes – especially for steel – also has an impact on the group’s direct GHG emissions, but is not an active decarbonization lever.

The main lever for mitigating upstream indirect GHG emissions is the targeted purchase of raw materials, materials and starting products with a lower carbon content than conventional products. In the case of downstream indirect GHG emissions, the main lever is the technological refinement of the product portfolio, especially in plant engineering. The goal is to deliver technologies that are themselves low-emission or facilitate lower emissions and, as result, enable customers to use production processes that emit less or no CO2 compared with conventional processes in their respective fields of application.

Investments, spending and financing the transition plan

The implementation of the transition plan for climate change mitigation is closely tied to the company’s financial planning. Some of the necessary CapEx and OpEx is financed from the company’s own capital resources – including for actions to increase energy and process efficiency or to switch third-party energy supply to renewable sources. Moreover, the implementation of some aspects of the transition plan is being funded by government grants, especially the construction of the fully hydrogen-capable DR plant in Duisburg for which funding commitments from the governments of Germany and North Rhine-Westphalia were already obtained in fiscal year 2022 / 2023.

To ensure consistent recording and reporting, the monetary assessment of the actions to implement the transition plan is based on the CapEx and OpEx definitions in the EU Taxonomy. In summary, this results in the following disclosures:

In the reporting year, operating expenditure (OpEx) for implementing the transition plan was around €8 million and capital expenditure (CapEx) around €104 million. The bulk of the capital expenditure – approximately €90 million– went to the ongoing construction of the hydrogen-capable DR plant in Duisburg. The capital expenditure associated with switching various productions steps to low-steel carbon production is also reported as part of the CapEx plan in accordance with the EU Taxonomy. The goal of the CapEx plan is to enable low-carbon steel production by thyssenkrupp in accordance with the criteria defined in Delegated Regulation (EU) 2021/2139. For the period from fiscal year 2025 / 2026 to fiscal year 2029 / 2030, cumulated expenditure of around €1billion is envisaged for further implementation of all decarbonization measures in the transition plan.

Locked-in risks and emissions-intensive assets

thyssenkrupp analyzes central assets – especially installations, the associated operating processes and the product portfolio – in respect of existing greenhouse gas emissions and those expected in the future throughout their entire life cycle or customary period of use. These are known as locked-in emissions. The focus is on the company’s carbon-based steel products and the use of the technical installations sold by the Decarbon Technologies segment in the downstream value chain.

As steel production is the main driver of emissions within the company’s own operations and plant engineering is the main driver of emissions in the upstream and downstream value chain, the transition plan defines specific focuses for reducing emissions in these emissions-intensive core areas. Therefore, these emission hot spots are considered in both the risk and resilience analyses. The time horizons used in the analysis are the same as those used in the assessment described in subsection “ESRS 2 SBM-3” and extend from the reporting year to 2030 and 2050, respectively.

It should be noted that the decarbonization levers of the transition plan – especially the establishment of hydrogen-capable steel production and the adaptation of the product portfolio to CO2-reduced products and technologies that are themselves low-emission or facilitate lower emissions – are aimed at reducing GHG emissions and may serve as the basis for achieving the intermediate GHG reduction targets and the long-term target of net zero emissions by 2050. Further information can be found in subsections “ESRS 2 SBM-3,” “E1-4” and “E1-6” in this section.

Paris-aligned Benchmarks

thyssenkrupp is not excluded from the Paris-aligned Benchmarks because the proportion of relevant sales in total net revenue – as defined by the exclusion criteria in Article 12 (1) (d) to (g) and (2) of Delegated Regulation (EU) 2020/1818 – is below the thresholds for this purpose.

Integration in the business strategy and approval by the management bodies

The transition plan is an integral element of thyssenkrupp’s corporate strategy, which is aimed at achieving profitable and sustainable growth. Therefore, the green transformation is one of the central strategic areas of action, alongside portfolio and performance. The anchoring of the transition plan is particularly evident from the fact that business models focus on decarbonization. One example can be found in the Decarbon Technologies segment, which consolidates the provision of key technologies for low-emission industrial production. These include technologies for the production of renewable hydrogen, for the CO₂-reduced production of cement (compared with conventional processes) and for concepts for CO₂-reduced basic material and chemical industries. This strategic alignment enables the company to reduce indirect GHG emissions in the downstream value chain and, at the same time, access the market potential harbored by the industrial transition to a sustainable economic system.

The Executive Board gave its formal approval to the transition plan in the 2024 / 2025 reporting year. Also in the 2024 / 2025 reporting year, the Supervisory Board then integrated new climate-related targets based on the transition plan into the long-term compensation for the Executive Board and top-level management.

Progress in implementing the transition plan

One key aspect of progress in implementing the transition plan has been the definition of medium- and long-term GHG reduction targets, including the target of achieving net zero emissions groupwide by 2050. The target was formalized in fiscal year 2023 / 2024 in an official declaration submitted by the Executive Board of thyssenkrupp AG to SBTi.

Further progress was made in the construction of the DR plant in Duisburg, which is the main decarbonization lever for GHG emissions in the company’s own operations. Following approval of the capital resources for this investment by the thyssenkrupp Executive Board and Supervisory Board in fiscal year 2021 / 2022, the dismantling work and preparation of the site were completed. The first steps in the construction of the DR plant have been ongoing since fiscal year 2023 / 2024. Further information on progress in constructing the DR plant can be found in the “Report on the economic position.”

Progress was also made in respect of the energy efficiency decarbonization lever. thyssenkrupp has been operating its Groupwide Energy Efficiency Program (GEEP) since fiscal year 2012 / 2013 and the progress achieved is reported each year. In fiscal year 2024 / 2025 efficiency measures made it possible to achieve energy savings of 162 GWh, which is equivalent to a reduction of 75 kt CO2e.

Moreover, the proportion of electricity used that came from renewable sources was also increased. In the 2024 / 2025 reporting year, 621 GWh of electricity came from renewable resources, which cut emissions by 77 kt CO2e year-on-year. Additionally, the company used 27 GWh of renewable energy it had generated itself, enabling a further reduction of 6 kt CO2e in GHG emissions.